How to Gain Good Credit and Unlock True Financial Freedom

Learning how to gain good credit is one of the most empowering financial moves you’ll ever make. Without strong credit, you face higher interest rates, frequent denials, and roadblocks to basic goals like buying a home, leasing a car, or even landing a job.

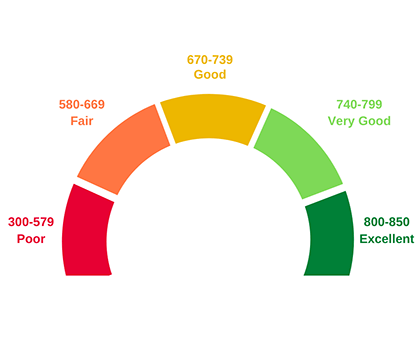

If your credit score feels more like a barrier than a badge of trust, you’re not alone. What’s worse—most people unknowingly follow outdated advice or take steps that actually slow their progress.

This guide will walk you through the most effective, modern-day techniques to build and maintain excellent credit—no guesswork, no fluff, just what works.

Credit Score First Principles: What Really Moves the Needle

Before diving into tactics, it’s vital to understand what drives your score. Here’s a quick breakdown of the five major components that impact your creditworthiness:

-

Payment history (35%): Timely payments are non-negotiable.

-

Credit utilization (30%): Using less than 30% of your available credit is ideal.

-

Length of credit history (15%): Older accounts are better.

-

Credit mix (10%): A blend of credit cards, loans, etc., helps.

-

New credit inquiries (10%): Too many applications can temporarily reduce your score.

Armed with this structure, let’s now look at the most impactful steps to raise your score quickly and sustainably.

Step 1: Start with the Credit Builder’s Toolkit

If you’re starting from scratch or repairing damaged credit, get these foundational tools in place:

1.1 Apply for a Secured Credit Card

This type of card requires a deposit, which acts as your credit line. Use it for small, regular purchases and pay it off in full each month.

1.2 Become an Authorized User

Ask a family member with great credit to add you to their account. Their on-time history and low utilization will boost your profile—without you even using the card.

1.3 Use a Credit-Builder Loan

Some credit unions and fintech services offer small installment loans designed specifically to build payment history. The money is often held in a savings account until repayment is complete.

Step 2: Optimize Credit Utilization Like a Pro

Keeping balances low relative to your total credit limit is one of the fastest ways to raise your score.

How do I lower my credit utilization?

-

Pay before the statement closes – not just before the due date

-

Ask for a credit limit increase – without increasing spending

-

Spread charges across multiple cards – instead of maxing one out

Pro Tip: Aim for under 10% utilization for optimal impact—not just the widely recommended 30%.

Step 3: Build a History That Speaks for You

The age of your credit accounts influences how lenders view your financial maturity. Here’s how to use this to your advantage:

-

Never close your oldest account, even if you don’t use it often

-

Keep dormant cards active with small auto-pay charges

-

Use accounts strategically to lengthen your average account age over time

The longer your credit timeline, the more reliable you appear.

Step 4: Protect Your Profile from Dings and Drops

A single late payment or aggressive application spree can undo months of good behavior. To avoid accidental damage:

-

Set autopay for minimum payments on all accounts

-

Use calendar reminders for larger bills

-

Avoid applying for too many credit cards in a short time

-

Regularly monitor your credit report for errors via AnnualCreditReport.com

Step 5: Tactically Diversify Your Credit Mix

Lenders want to see how you handle different types of credit. This doesn’t mean you should take out loans you don’t need, but a healthy mix strengthens your score.

Types of credit to consider:

-

Revolving credit: credit cards, lines of credit

-

Installment credit: auto loans, student loans, mortgages

Note: It’s not necessary to have all types—just a thoughtful blend that demonstrates responsibility.

Smart Moves for Fast Credit Improvement

Can you improve credit in 30 days?

Yes, but results depend on your current situation. Key strategies include:

-

Paying down high balances

-

Removing errors via dispute

-

Becoming an authorized user

-

Requesting rapid rescoring from lenders (in special circumstances)

Should you pay off all cards completely?

Paying cards down to zero helps utilization—but keeping a small balance (1–3%) reported can sometimes be beneficial for score optimization.

What to Do if You’ve Made Credit Mistakes

Mistakes happen. What matters is how you recover:

-

Late payments: Contact the issuer and request a goodwill adjustment

-

Collections: Negotiate a “pay-for-delete” if possible

-

Charge-offs: Pay or settle, then rebuild with positive behavior

Disputing errors:

File with the credit bureau reporting the error. Include supporting documentation and check for resolution within 30 days.

Advanced Credit Strategies Few People Talk About

Leverage Rent Reporting Services

Use platforms like RentTrack or Experian Boost to have your on-time rent or utility payments reported to credit bureaus.

Stagger Card Payment Dates

By having different statement closing dates across multiple cards, you can keep reported utilization consistently low—even while using your cards regularly.

Optimize for FICO vs. VantageScore

Different lenders use different scoring models. Most major decisions (like mortgages) rely on older FICO versions. Knowing this can help tailor your efforts.

Final Thoughts: Credit is a Long-Term Asset, Not a Short-Term Fix

Mastering how to gain good credit isn’t just about boosting a number—it’s about building leverage in life. With great credit, you qualify for better rates, gain negotiating power, and access doors others can’t even knock on.

It starts with one card. One payment. One small win. But the ripple effect compounds.

Tonka Bluebird

Author

Tonka is part of the Navajo tribe and has an advanced master degree in finance and economics and has been in the financial industry for over two decades and brings that knowlefe and experience to our blog.